I had written an article on why Senior Citizens should look to invest in Equity Oriented Schemes (with some formula & strategy) on January 20’2015 both on Misterbond & in Wealthforum.

This article was well received & appreciated (which can be judged by number of mails I received; besides the comments appearing below this article by many IFAs).

However, one query which was posted on my website is how this strategy could have worked in all market conditions.

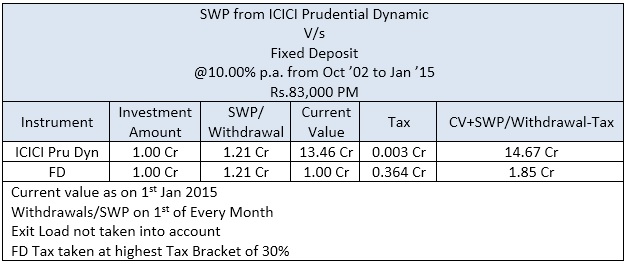

I had given one example of ICICI Prudential Dynamic Scheme- SWP from the same @10% p.a. since 2002 (since inception of the scheme). As rightly pointed by one of the readers that markets have done extremely well since 2002 & hence the following result (I am reproducing that example for the benefit of the readers):

As can be seen from the above table; inspite of withdrawals of Rs.1.21 crores since October 2002 to January 2015; value of the said scheme was Rs.13.46 crores. This got me thinking & thought of applying this strategy on the same scheme for starting every year since 2002 i.e. I have shown below outcome of this strategy if one would have invested & opted for this strategy starting either 2002 or 2003 or 2004, so on & so forth.

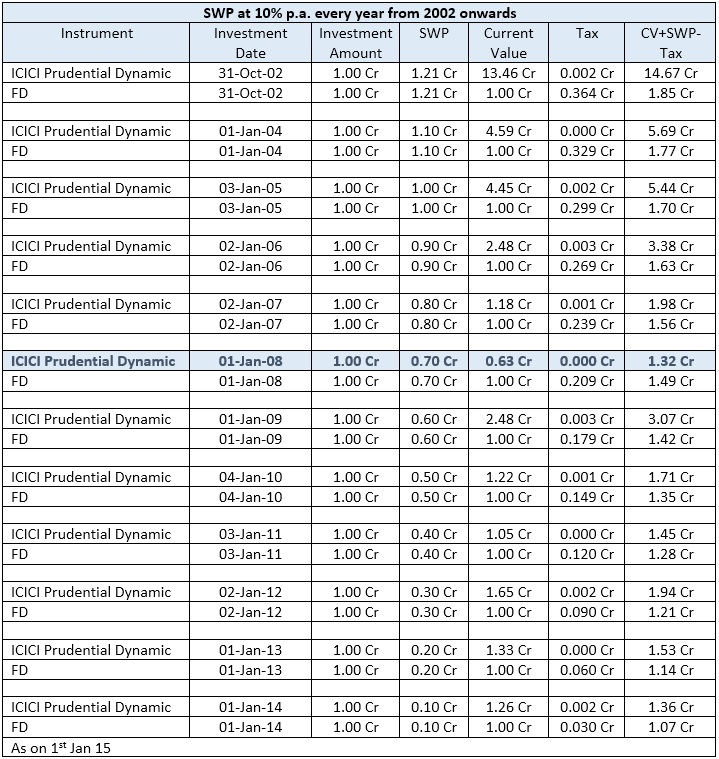

Outcome is for everyone to see & appreciate. Since 2002, if a senior citizen would have opted for this strategy , in almost all years (except of course starting year of 2008), even after the withdrawals, current value of original investment (Rs.1 crore) is higher than the original investment value – lowest being Rs.1.05 crores & highest being Rs.13.46 crores as shown above.

Only if a senior citizen would have opted for this strategy in January 2008, after withdrawals of Rs.70 lacs, current value is Rs.63 lacs against original investment value of Rs.1 crore. This is for obvious reasons of dipping into the principal amount even in the year when markets corrected by almost 60% in one year from its peak achieved in January 2008. However, if the said investor continues & pursues the said strategy; possibility is that at some point this drop in valuation will be halted & start to grow.

As I had mentioned in my original note, cash flows of the senior citizen is not affected. Risk of principal erosion will be borne by the beneficiaries. Hence, this strategy has great merit as out of 12 years, only adopting the said strategy in the year 2008 till date has eroded principal amount.

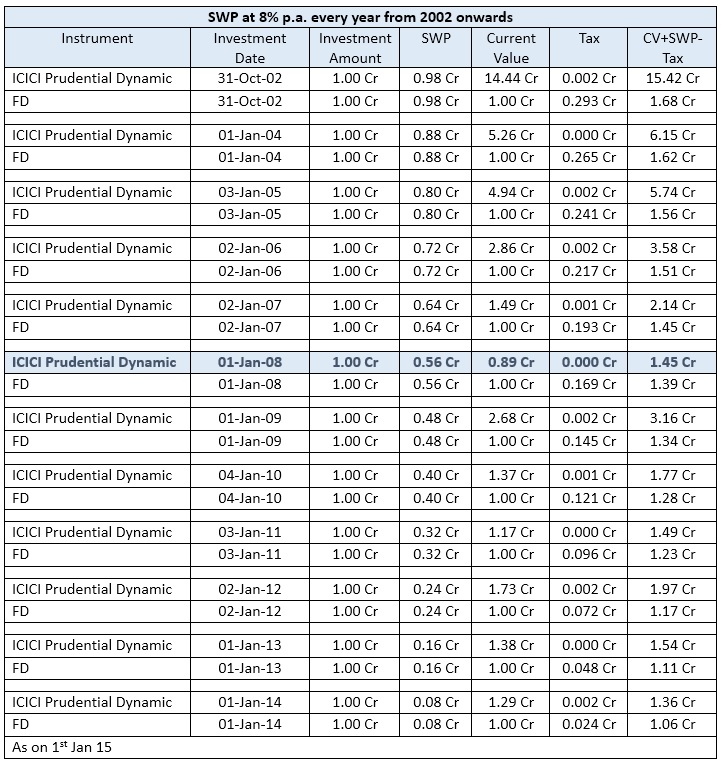

Lesson learnt from these examples is that in a pure bearish market trends or as a strategy, maybe the investor could have opted for lower SWP (maybe 7-8% instead of 10%). At 8% SWP from year 2008, current value of original investment would have been Rs.89 lacs (v/s Rs.63 lacs under 10% SWP since 2008) & at 7% SWP current value of original investment of Rs.1 crore would have been Rs.1.04 crores. Also, please note that these SWPs at either 7% or 8% do not attract any significant tax outflows v/s same returns attracting between 20-30% tax outflows if the Senior Citizens had opted for investments in FDs. Going forward returns in FDs will start coming off as RBI would be cutting interest rates over next 1 year or. Hence pretax & post tax returns would be on much lower side going forward.

Another query that was posted was whether the investor should keep 10% in say liquid scheme, create SWP from this folio & let balance 90% be invested in equity or equity related schemes. This way investor does not dip into principal in the first year but let’s 90% funds grow & starts SWP from equity from 2nd year onwards.

Another query that was posted was whether the investor should keep 10% in say liquid scheme, create SWP from this folio & let balance 90% be invested in equity or equity related schemes. This way investor does not dip into principal in the first year but let’s 90% funds grow & starts SWP from equity from 2nd year onwards.

This strategy, according to me has two flaws: 1) 10% of the funds will be depleted in 1st year itself as the investor would create 2 folios viz. 10% in liquid & 90% in equity. In the first year 10% in liquid will become zero by the end of the year & 2) here we are assuming that equity portfolio will grow over next one year & your 90% equity portfolio will appreciate during this period. What if equity markets correct during this period (say like the year 2008-2009). Will the investor have the heart to continue investments in the said equity scheme/s & further have the heart to create SWP on depleted amount lying in the said portfolio. In all probability, he may even get out of the entire portfolio alongwith the strategy & never return again to this asset class.

Hence, as they say, you can never time the markets either on entries or exits. If you create long term strategy for senior citizens, with lower SWP than say 10% as mentioned earlier, in all probability even in worst periods the investor will not lose much even after these SWPs. At 8% SWP in the said scheme from 2008 onwards, current value of original Rs.1 crore would be down to 89 lacs (post SWPs). In the example above of 10:90 in favor of liquid: equity, post first year SWP your original portfolio is already down to 90% (not considering +/- on equity portfolio).

Hope this sequel to my original note will help IFAs to convince senior citizens to invest in Equity Oriented schemes rather than FDs for their retirement cash flow planning.

Conclusion:

There is huge opportunity for all IFAs to start providing solution for retirement cash flow requirements & move funds from traditional mindset. Also, this strategy helps 2 generations of investors viz. a) retired senior citizens to meet their daily cash flow requirements during their lifetime alongwith an opportunity to grow their corpus (v/s eroding the same in terms of purchasing power due to impact of inflation – as explained in my first note) & enjoy their GOLDEN YEARS & b) benefit the beneficiaries by letting investments grow over a period of time.

Follow me on twitter : @IamMisterBond